Yields for newly issued Certificates of Deposit [CDs] change regularly. One factor that has an indirect but outsized impact on these yields is the Fed funds rate. Businesses that understand the relationship between the Fed funds rate and CD yields can purchase CD investments at an opportune time and keep their reserve cash working.

How does the Fed funds rate impact CD yields?

Banks have some autonomy when setting the rates that they pay for CDs. However, there are many external factors that influence these rates including bank revenue, yields for debt investments, and consumer expectations. The Fed funds rate impacts all three of these factors and therefore indirectly affects CD yields.

Bank Revenue

As the Fed funds rate rises, many of the country’s interest rates follow – including bank loans. When banks earn more revenue from loans, they can afford to pay businesses more for their CD investments. Conversely, when the Fed funds rate falls, banks earn less from their loans and tend to reduce the rates they pay for CDs.

Returns for Debt Investments

Like other forms of debt, bond yields are highly sensitive to changes in the Fed funds rate. Because bank CDs often compete with bonds, the rates for the two investments tend to move similarly.

Consumer Expectations

Changes to the Fed funds rate impact consumer expectations. When this rate rises, depositors expect their investments to yield more, and banks often raise the rates they pay for CDs. On the other hand, when yields are falling nationwide, depositors expect less income from their investments and banks tend to lower CD yields.

How closely do CD yields mirror the Fed funds rate?

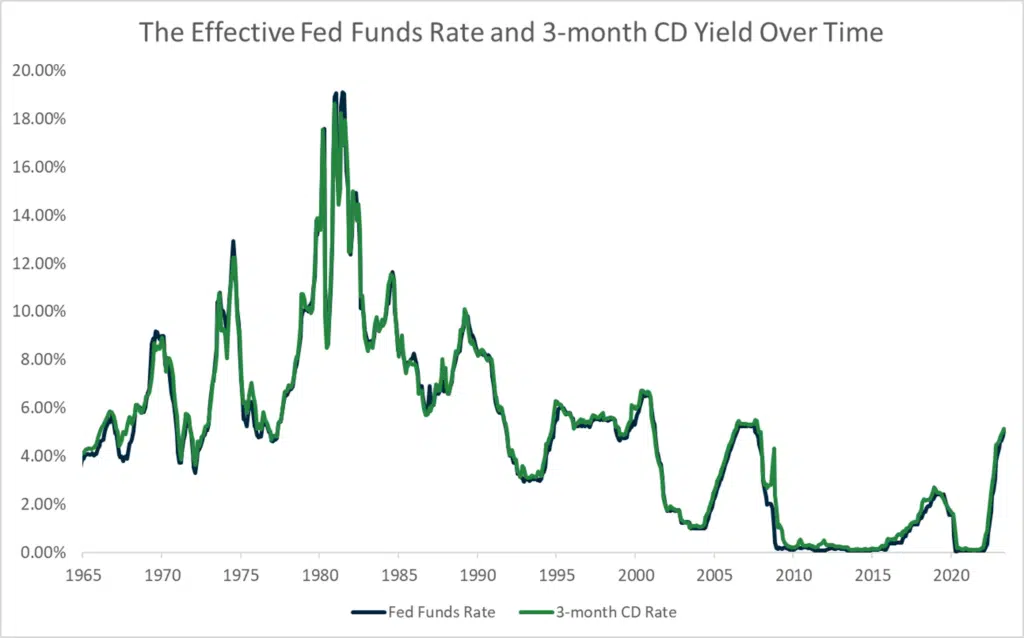

The Fed funds rate sets somewhat of a baseline for CD yields. Then, other factors – like risk – determine the yield for specific CDs. The Fed funds rate has historically had the strongest correlation with low-risk CDs. In fact, the national average rates for 3-month CDs have moved almost in tandem with the Effective Fed Funds Rate since 1965.

In the chart below, the blue line represents the Effective Fed Funds Rate, and the green represents the average 3-month CD yield. As you can see, these two rates have moved almost in lockstep for nearly sixty years.

Data sources: Effective Fed Funds Rate: FRED. 3-month CD Rates: FRED.

Other Factors that Impact CD Rates

Outside of the Fed funds rate, there are several factors that influence CD yields. As previously mentioned, risk is one of these factors. Additionally, individual bank needs can lead CD rates to vary significantly in different areas and between different banks.

How Risk Impacts CD Yields

Longer-term CDs have increased interest rate, inflation, and opportunity risk. For this reason, CDs with longer terms generally have higher yields than shorter-term options. However, when interest rates are rising, these risks can be heightened and demand for long-term CDs can fall. While rare, these changes in demand can lead to an inverted yield curve where shorter-term CDs have higher yields than longer-term options.

Individual Bank Needs Can Influence CD Yields

The rates that each bank offers for CDs can vary greatly depending on the individual needs of the bank. When banks have enough deposits to fund their lending activity, they don’t need to attract new depositors. For this reason, they may pay below average yields. On the other hand, banks that need to attract new depositors tend to raise the rates they pay above the competition.

Because yields can vary dramatically between banks, it is difficult to know if you are getting a competitive rate from your local bank. Fortunately, advances in financial technology – a.k.a. fintech – mean businesses no longer need to monitor rates from hundreds of banks to achieve a competitive yield. A fintech company that specializes in deposit management can help your business analyze current CD holdings, invest in new CDs with competitive yields, and even replace current CDs with higher yielding options.

Earn More, Risk Less® with CD Investments from ADM

As the Fed funds rate has risen, many businesses have found that their CD rates are far below the yield they could achieve with a new CD. Our company, the American Deposit Management Co. [ADM] can help. Our CD reinvestment program helps businesses capture higher yields, net of early withdrawal fees. Additionally, we offer a CD-term account which helps businesses access CDs from across the country.

ADM is not a bank. We are a fintech company that helps businesses achieve extended safety and competitive rates by spreading cash across our nationwide network of banks and credit unions that compete for deposits. We call this concept Marketplace Banking™ and it allows our clients to access extended FDIC / NCUA protection and nationally competitive returns.

To learn more, contact us today.

*American Deposit Management Co. is not an FDIC/NCUA-insured institution. FDIC/NCUA deposit coverage only protects against the failure of an FDIC/NCUA-insured depository institution.