What Corporate Leaders Must Know About the Deposit Insurance Fund

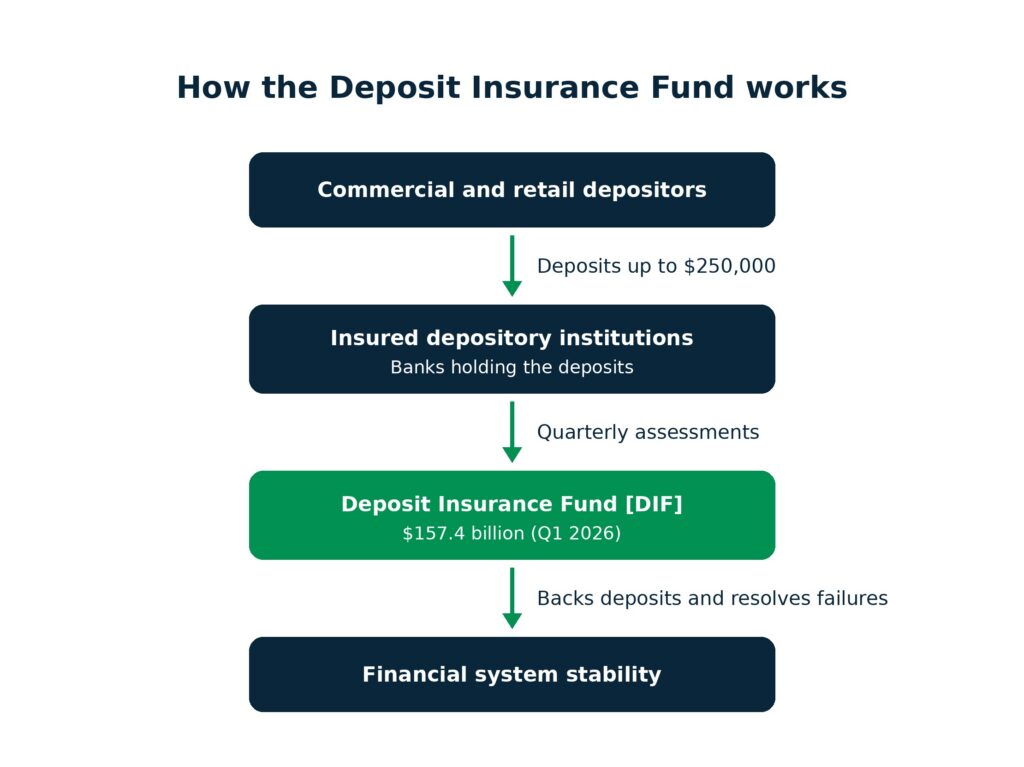

Smart treasury management goes beyond tracking internal cash flow – it means knowing whether the banks holding business cash are structurally sound. As commercial activity expands across the country, businesses are moving more working capital than ever, which raises the stakes on where they park it. The ultimate safety of business cash often rests on one mechanism – the Deposit Insurance Fund [DIF].

Consumers recognize the FDIC logo on the branch door, but executives need to look past the sticker. The DIF is the actual pool of capital backing those guarantees. By understanding this fund, business leaders gain real insight into systemic risk and where their liquidity is truly protected.

Decoding the Deposit Insurance Fund

The FDIC maintains the DIF to protect depositors and keep public confidence in the financial system. Congress created it during the Great Depression to stop the bank runs that were paralyzing the economy. Today, when an insured bank fails, the FDIC taps the DIF to get depositors their insured money without interruption.

Taxpayers don’t fund this safety net – the banking industry does. Insured banks pay quarterly assessments based on their liabilities and risk profile, and the fund earns additional income from the interest on its U.S. Treasury holdings.

To gauge the fund’s strength, the FDIC tracks one core metric – the reserve ratio. This is the DIF balance measured against all estimated insured deposits in the system. Federal law dictates the required ratio, so the amount that banks pay to operate is tied directly to macroeconomic shifts and the health of the overall economy.

The State of the DIF

A surge in deposits in early 2020 pushed the reserve ratio below the 1.35% statutory minimum by mid-year, forcing the FDIC into a strict Restoration Plan to rebuild the fund. To speed the recovery, the agency raised base assessment rate schedules by 2 basis points across the board, effective in 2023. That same year, regional banking stress tested the system and reinforced the reasons why a well-capitalized DIF matters.

The plan worked. Strong assessment revenue and normalizing deposits pushed the DIF back above its statutory minimum – ahead of schedule – letting the FDIC exit the Restoration Plan.

The recovery cleared only the near-term bar of 1.35%, but the FDIC’s standing target sits higher – at 2%. In fact, the Designated Reserve Ratio [DRR] has remained steady for more than a decade. The table below tracks the fund’s trajectory heading into mid-2026.

![Key Deposit Insurance Fund [DIF] Metrics. The table lists an increasing DIF balance and reserve ratio, in addition to the statutory minimum (1.35%) and reserve target (2%).](https://americandeposits.com/wp-content/uploads/dif-metrics-table-1024x474.jpg)

This data reflects a stabilizing banking environment, and the Q1 2026 balance of $157.4 billion should reassure depositors and business leaders alike. However, business leaders should keep a close eye on future data, because the fund only stays healthy as long as the banking sector keeps paying.

How the FDIC Calculates and Collects Assessments

The cost of funding the DIF shapes commercial banking, so it is important to understand it. The FDIC uses a risk-based system to set each bank’s contribution, so institutions that take on more risk pay higher premiums.

There are four components that drive the calculation:

- Assessment base: Instead of basing premiums on deposits alone, the FDIC uses average consolidated total assets minus average tangible equity, which gives a truer picture of a bank’s footprint.

- Risk categories: The FDIC sorts banks by supervisory ratings – like CAMELS scores and financial ratios – so higher-risk banks pay steeper rates.

- Base assessment rates: The FDIC sets the starting schedules. Community banking advocacy groups keep pushing to lower these rates for smaller institutions, but the 2 basis-point increase was applied uniformly to keep the fund growing toward the 2% DRR target.

- Adjustments: A bank’s final rate may be adjusted based on factors like its unsecured debt and funding mix.

The FDIC can also levy a special assessment under systemic pressure. For example, it did exactly that following the 2023 regional bank failures to recover the losses that were realized by protecting uninsured depositors. The agency aimed the special assessments at the largest and most interconnected institutions – sparing smaller community banks from carrying the bulk of the cost.

The Corporate Conundrum: Navigating the Cap

A healthy DIF brings peace of mind, but it doesn’t erase the system’s limits. FDIC insurance still caps out at $250,000 per depositor, per insured institution, for each account ownership category.

This ceiling covers most retail consumers, but it’s only a fraction of what a mid-sized or large company holds in its accounts. When a business parks millions in a single commercial checking account, everything above $250,000 relies on that bank’s health – rather than the multi-billion-dollar backing of the DIF.

Uninsured deposits leave decision-makers juggling three competing pressures:

- Concentration risk: Keeping cash under one roof simplifies treasury work but exposes the company to frozen or lost funds if that bank runs into trouble.

- Administrative burden: Chasing full coverage by opening and reconciling accounts at dozens of banks drains accounting and treasury resources.

- Yield sacrifice: Scattering cash across disconnected retail accounts weakens the company’s leverage to negotiate competitive rates on its total balance.

Each of these situations trades one weakness for another. No single-bank setup escapes the bind, because the FDIC insurance cap leaves large balances exposed no matter how a company arranges its accounts. The solution is a cash management system built for corporate-scale cash, not a retail account stretched past its purpose.

Strategic Cash Management in the Modern Financial Landscape

A single-bank setup forces a tradeoff between keeping cash safe and putting it to work. For large balances, leaning on basic bank accounts adds operational risk the company doesn’t need. To protect working capital without slowing daily operations, businesses need a smarter structure.

A modern treasury solution can spread cash across a network of well-capitalized banks, extending insurance coverage across the full balance without adding friction to daily workflows. The result: a company protects its entire balance and earns better yield while still managing everything through what feels like a single bank.

Secure Your Full Balance with ADM

The DIF protects the financial system, but the $250,000 cap still leaves large corporate balances exposed at any single bank. Smart treasury management closes that gap, and it does not require juggling dozens of accounts.

At American Deposit Management, we help businesses optimize their cash reserves. Our modern solutions provide access to extended government insurance that protects all of your business cash – not just the first $250,000.

Safety is only part of the value. Our nationwide network of financial institutions competes for your business deposits, which lets us offer nationally competitive returns. Your team also gains the convenience of next-day liquidity. To learn more about our modern cash solutions, contact a member of our team today.

How to Optimize Excess Corporate Cash in 2026

A CFO’s Guide to Balancing Yield, Liquidity, and Deposit Protection To optimize excess corporate cash in 2026, organizations should segment funds by liquidity need, compare…

How AI Is Transforming Corporate Treasury and Cash Management

AI now forecasts cash, flags fraud, and reconciles accounts in corporate treasury – but adoption remains in early stages.

FOMC June Meeting Summary: Stable Rates, Sweeping Institutional Reforms

The June FOMC meeting marked Kevin Warsh’s first as Chairman, with a rate decision and sweeping reforms to Fed practices.