How a Nationwide Deposit Network Strengthens Community Banks and Credit Unions

Community banks anchor lending in thousands of towns across the U.S., yet most gather deposits from a single market. That mismatch creates a structural disadvantage, where loan demand can outgrow the local deposit base. Further, national competitors can reach those same depositors with nationwide ads or even a quick phone call.

On the other hand, a modern strategy that leverages a nationwide deposit network gives community banks a way to close that gap. Get started by understanding how a local funding strategy often falls short, and how the network model turns geography into an advantage – rather than a constraint.

The Funding Challenge Facing Community Depository Institutions

A community bank or credit union’s greatest strength is often its deep roots in a single market. Unfortunately, this same advantage also defines its funding ceiling. Since traditional deposits come from the households and businesses within driving distance of a branch, there is a limited amount of funds available. When loan demand outpaces that local base, the bank must slow lending, raise rates, or turn to wholesale funding.

Cash concentration within local markets further compounds the problem, as the same local economy feeds both sides of the balance sheet. This means a downturn in a dominant regional industry can both weaken loan performance and shrink deposits at the same time. Agricultural towns see this in poor harvest years. Energy markets see it when commodity prices fall. Seasonal economies see it every year as tourist dollars rise and fall.

Competition – both inside and outside an institution’s service area – adds a third pressure. Money center banks, online banks, and consumer fintech platforms now court local depositors with national rate sheets and polished digital tools. Then, it only takes a few minutes for a business owner to move operating cash out-of-state. Fortunately, community banks built on relationships still win loyalty. However, loyalty alone rarely holds a large balance against a meaningful rate gap.

Finally, the traditional answer of building more branches moves too slowly and costs too much to solve a funding shortfall that is measured in quarters rather than decades. That’s why community banks need a faster way to reach deposits beyond their home market – a nationwide deposit network provides the answer.

How a Deposit Network Works – and What It Delivers

A deposit network flips the geography problem. Instead of waiting for deposits to walk through the door, a participating bank or credit union receives funds gathered from depositors across the country. The result is a reliable deposit stream for banks, with nationwide depositor demand that transcends the local economy.

What is a Deposit Network?

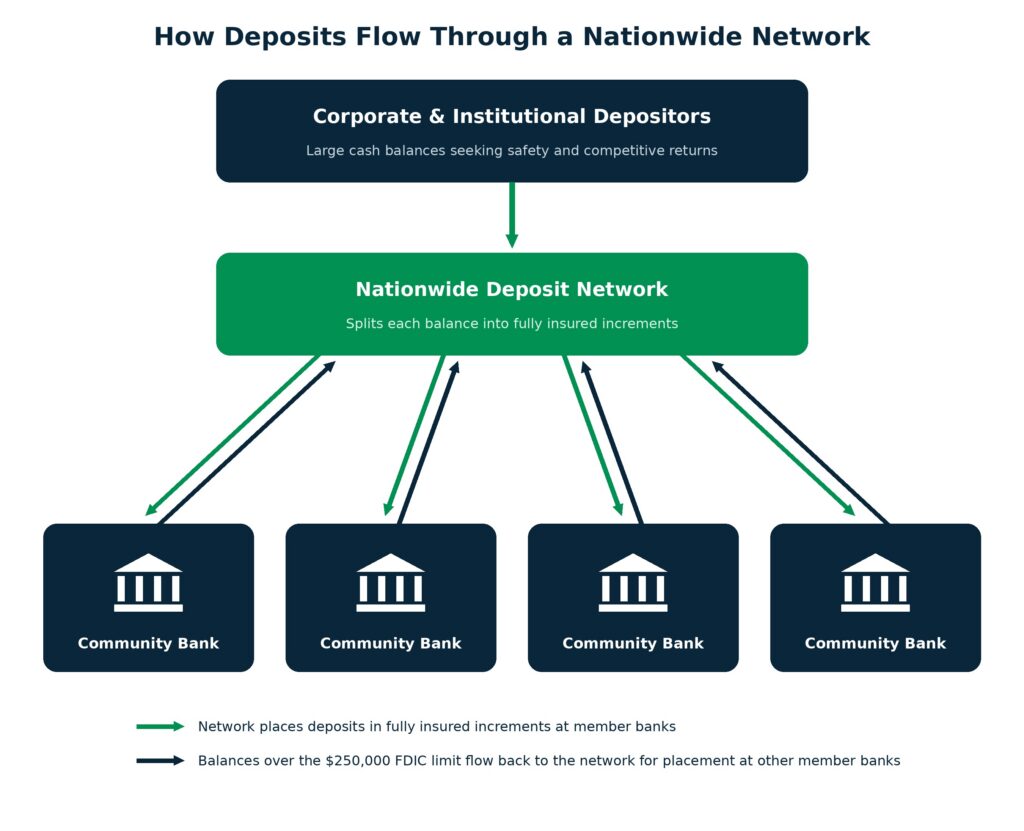

A deposit network connects two groups with matching needs. On one side, banks want stable funding. On the other side, businesses, institutions, and public entities with large cash balances want safety and access to a nationally competitive return.

The deposit network solves both issues by placing depositor funds across its member banks, spreading each depositor’s balance, so that every dollar stays within federal insurance limits and earns a competitive return.

With the right network, cash can flow in either direction or maintain stable liquidity while providing additional FDIC or NCUA protection. A bank or credit union sends its own large customer deposits into the network and receives matching deposits back from other members.

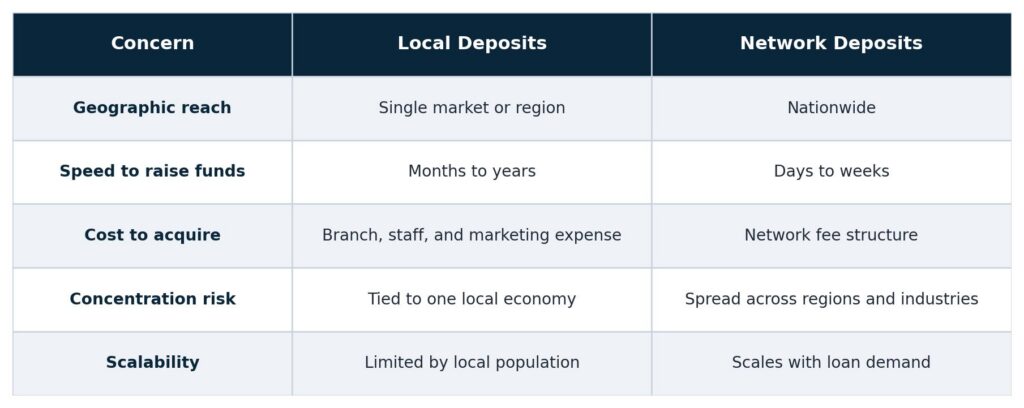

The table below compares the two approaches to deposit gathering.

What Banks Gain

Funding diversification leads the list. Network deposits originate from depositors in many states and industries, so a slump in the bank’s home market no longer drains its funding at the worst possible moment.

Liquidity management improves next. A bank can take on network deposits when loan pipelines fill and let them roll off when demand cools. That flexibility beats overbuilding a branch footprint for peak demand that arrives only occasionally.

Cost efficiency follows. Reaching new depositors through a network requires no new branches, no expanded marketing budget, and no out-of-market staff. The bank pays for funding it actually uses.

Stability rounds out the case. Relationship-based network deposits behave differently from rate-listing money that chases the highest posted yield each month. Depositors who choose a network for safety and service tend to keep balances in place, which gives bank treasurers a funding source they can plan around. Network participation also opens the door to large corporate balances that would otherwise default to money center banks.

Why Depositors Keep the Network Strong

A funding source only works if the money keeps coming, and depositor incentives keep it coming. Large depositors face a real problem – federal insurance covers $250,000 per depositor, per bank, per ownership category. A company holding $10 million in operating cash cannot protect that balance at a single institution without leaving most of it exposed. A deposit network solves that problem by spreading the balance across many member banks, which extends full federal protection to the entire amount. Add competitive nationwide returns and a single relationship to manage, and the value to the depositor becomes clear.

The result is a self-reinforcing system. Depositors gain protection and yield. Banks gain stable, diversified funding. Each side’s demand strengthens the other, which keeps the network reliable through varying rate cycles.

Regulatory and Risk Considerations

Network deposits carry regulatory nuances that bank leaders should understand before signing on, and classification is the most important. Regulators distinguish between core deposits and brokered deposits, and the label affects how examiners view a bank’s funding profile.

Congress addressed part of this question in 2018. The Economic Growth, Regulatory Relief, and Consumer Protection Act allows well-capitalized banks to treat reciprocal deposits as non-brokered up to the lesser of $5 billion or 20% of total liabilities. The FDIC further revised its brokered deposit framework in a rule that took effect in 2021. This rule clarified when third-party placement arrangements fall outside the brokered category.

Due diligence completes the picture. Before joining a network, a bank should evaluate the operator’s track record, the composition and behavior of its depositor base, the fee structure, the technology and reporting tools, and the contractual terms that govern deposit flows. After all, a deposit network is a funding partner, and it should vetted with the same rigor that is applied to any other counterparty.

Banks that work through these questions have positioned themselves to use network funding with confidence. They’ll also have the knowledge to explain that funding clearly to their examiners and boards.

The AMMA Network – A Deposit Network Built on Community Financial Institutions

At American Deposit Management [ADM], we built our deposit network to support community banks and credit unions. It starts with our American Money Market Account [AMMA], which connects corporate and institutional depositors across the country with our nationwide network.

For participating banks and credit unions, AMMA Exchange™ delivers deposits and balanced liquidity options, while high-value depositors receive access to full federal protection for their cash. ADM’s team manages the placement, the reporting, and the depositor relationship, which allows bank and credit union staff to focus on lending and local service.

Our team works directly with each depositor and each bank. This model produces funding that behaves like the stable deposits that community banks want on their balance sheets. If you are interested in our modern cash solutions, contact our team.

Best Cash Management Solutions for School Districts and Local Governments to Optimize Excess Cash

Municipalities and school districts are often responsible for managing millions of dollars in public funds. Whether those balances come from operating reserves, bond proceeds, referendum…

How to Optimize Excess Corporate Cash in 2026

A CFO’s Guide to Balancing Yield, Liquidity, and Deposit Protection To optimize excess corporate cash in 2026, organizations should segment funds by liquidity need, compare…

How AI Is Transforming Corporate Treasury and Cash Management

AI now forecasts cash, flags fraud, and reconciles accounts in corporate treasury – but adoption remains in early stages.